A home is a fundamental commodity designed for ‘living.’ If the financial pressure on affluent property owners is heightened by increasing real estate taxes, this expense will eventually be transferred to renters, potentially causing an increase in housing costs.

Shin Seong-hwan, a former member of the Bank of Korea’s Monetary Policy Committee who finished his four-year term last month (May), recently expressed in an interview, “I doubt if taxing unrealized gains is suitable for controlling housing prices,” and noted, “Historical evidence indicates that the negative consequences were more significant.” As an expert in finance and economics with experience in both academic and practical settings, Shin collaborated with former BOK governors Rhee Chang-yong and Shin Hyun-song on the Monetary Policy Committee before resuming his role as a professor in the Department of Business Administration at Hongik University. His replacement is Kim Jin-il, an economics professor at Korea University.

Shin was more open about the South Korean economy in the interview than he was while serving on the Monetary Policy Committee. He highlighted major issues facing the economy, including significant polarization, high savings levels, and shifts in exchange rate factors compared to previous periods.

◇ “Previous Increases in Property Taxes Only Led to Higher Home Prices”

-What would be your assessment of the present condition of the South Korean economy?

In short, only the positive sectors are performing remarkably. The semiconductor industry has found a goldmine because of the AI surge. Unlike a lottery, which is a single occurrence, the semiconductor growth is anticipated to continue for another one or two years. This ‘highly successful sector’ is influencing growth rates and prices broadly. However, the ‘spillover effect’ from this success is significantly less than in the past. The heat from the semiconductor goldmine is not effectively reaching other parts of the economy.

-Why is the trickle-down effect not strong?

Since the booming industries are all very capital-heavy, even with significant investments from semiconductor firms, the impact on job creation—which typically results in a faster spread of benefits—is minimal. The government’s tax income has risen, and the stock market is doing well, yet the system is structured in a way that it will take time for every citizen to benefit from these gains. Moreover, it remains unclear if the ‘negative consequences’ of this sudden wealth, like real estate price bubbles, can be managed.

The conversation with Shin occurred against the backdrop of worries that the influx of capital into the market, fueled by the semiconductor industry’s success, might enter the real estate sector, pushing up home prices. The government suggested increasing property taxes on housing—a subject that had been off-limits for a long time—on the 21st, as housing prices began to show signs of becoming too high, leading to debate.

-What do you believe is the reason behind real estate prices staying persistently elevated?

If there are buyers but no suppliers, prices are bound to go up. The government states it is boosting supply, but for this to work, it needs to offer attractive housing in areas with high demand, like revitalizing central Seoul which is well-connected. However, these regions involve numerous powerful interests and regulations, leading to a lengthy development process. As a result, the government has to construct homes in less sought-after areas using tax funds to meet its housing supply goals during its term.

-How about increasing property taxes to reduce demand?

It could have a short-term impact, but I don’t consider it a long-term answer. The aim of increasing property taxes is to lower housing demand and keep prices steady by making ownership more expensive. However, housing is a necessary item with the primary function of providing a place to live, so there are boundaries to how much demand can be reduced. The advantage of owning a home, which eliminates future housing cost uncertainties like jeonse or monthly rent, continues to drive interest in property ownership.

-There are reasons to raise the tax burden on extremely expensive properties.

Past experiences indicate that as property taxes increase, homeowners transfer the additional tax burden to renters. This results in higher jeonse and monthly rent, which ultimately causes housing prices to rise. Although increasing property taxes may be essential for government revenue, I wonder if imposing taxes on unrealized gains is a suitable policy to control housing prices. I believe it’s important to consider other countries’ examples when addressing tax matters.

◇Exchange Rates Influenced by the Stock Market: “A Unique Situation”

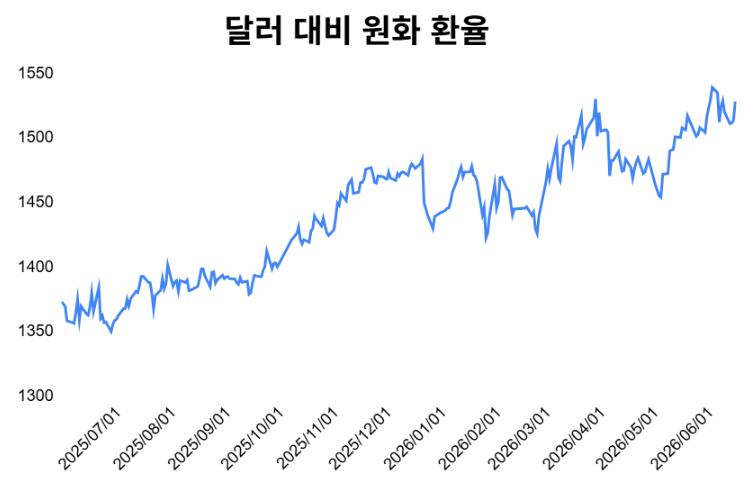

-Why hasn’t the high exchange rate become stable since the latter part of last year?

Although the dollar remains strong, South Korea’s high exchange rate is also influenced by substantial capital outflows. Citizens are purchasing dollars and investing overseas, arguing that there are more lucrative opportunities in the U.S., while non-residents are converting their large short-term profits from local stock investments into dollars and bringing them back. First, examine citizens’ investments abroad. The U.S. offers higher potential growth rates compared to Korea, and its interest rates are higher. This trend is anticipated to persist, so ‘ants heading west’ continue to invest in the U.S.

Professor Shin stated, “The exchange rate problem resulting from non-residents selling Korean stocks is a unique situation.” In recent times, foreign investors have been significantly selling Korean stocks, converting won into dollars, which has led to an increase in the stock market while the value of the won decreases (exchange rate increases). Major global institutional investors establish fixed investment proportions by country. As the Korean stock market experienced a surge, increasing its proportion in their portfolios, they sold Korean stocks based on their guidelines. Shin explained, “The fact that Korea’s growth rate is increasing and its stock market is performing exceptionally well is prompting foreign investors to adjust their portfolios, resulting in depreciation of the won. This is a situation that contradicts traditional exchange rate theory and is worth further study.”

-Can higher levels of foreign investment in South Korea affect the exchange rate?

Obviously, the heightened interest from international investors in South Korea’s financial market is positive. Nevertheless, given that the won is not a reserve currency, the government must develop foreign exchange market stabilization strategies to manage market saturation. This is akin to how high-performance vehicles require enhanced safety features like improved airbags and braking systems.

-Is there anything that foreign exchange authorities can do to stabilize the high exchange rate?

There are limited effective methods to maintain market confidence that the won will continue to appreciate. To ease market sentiment, authorities need to instill a sense of fear: ‘The government can step into the foreign exchange market at any moment, and those who bet against its position will face significant losses.’ At present, this kind of policy pressure is not evident. If the high exchange rate continues, it will lead to increased import costs, followed by higher consumer prices, directly affecting the public, particularly self-employed people and small businesses. Last year, the government sought to prevent the exchange rate from exceeding a certain threshold and achieved some success. However, after the Middle East conflict pushed the rate to 1,500 Korean won, the government’s vigilance decreased, allowing the high exchange rate to become entrenched.

– Officials in foreign exchange claim that the ‘1,500 South Korean won exchange rate’ is excessively high given Korea’s economic framework.

I concur. Fundamentals indicate this, but markets are not solely driven by fundamentals. In the current scenario, where financial markets overshadow the real economy, market trends are particularly significant. The real economy progresses steadily over time, but financial markets are difficult to correct once they become one-sided without a ‘counterbalance.’ Last year, the National Pension Service’s foreign exchange swaps served as a counterbalance, but with residents’ investments pushing the exchange rate higher, the government now has limited choices. As Korea’s capital market becomes increasingly reliant on foreign investors—due to the inclusion of Korean government bonds and stocks in the WGBI and MSCI developed market indices—the influence of market concentration will increase.

-What is your assessment of the recent increase in the Korean stock market?

The level of concentration is excessively high. Samsung Electronics and SK Hynix contribute approximately 80% of the operating profits of all listed companies. With these two stocks representing more than half of the market capitalization, the KOSPI cannot be viewed as a well-diversified, suitable portfolio. This is a matter that financial regulators and the Korea Exchange need to tackle. The rationale behind investing in indices such as the S&P 500 is based on the belief that they are well-diversified. The KOSPI has evolved into a market where index investing is no longer justifiable. Due to the extreme concentration, volatility is significant. The market often experiences sharp rises and drops, causing circuit breakers to activate and daily fluctuations of 7–8%. This is not typical.

During his last term on the Monetary Policy Committee last year, Shin presented five ‘rate cut’ minority views in meetings where the BOK maintained interest rates. He advocated for proactive actions against potential economic slowdowns when there was still room to reduce rates. The BOK has kept rates steady since May of last year, but with the won’s exchange rate increasing and inflation climbing, rate cuts are no longer feasible. Governor Shin Hyun-song has effectively indicated a possible rate increase next month. At his final meeting last month, Shin stated, “Even if the economy faces difficulties, minimizing inflation shocks is an important responsibility of the BOK.”

◇”Koreans Live Poorly and Die Rich”

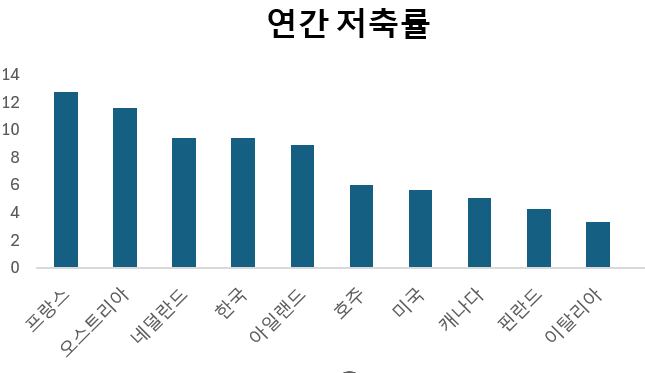

He also highlighted Korea’s unusually high savings rate as an issue that requires attention, drawing from his experience on the Monetary Policy Committee. The savings rate reflects the amount of disposable income remaining after households have spent on consumption. In 2024, Korea’s household savings rate stood at 9.4%, ranking eighth among 30 OECD nations. When including the corporate and government sectors, the overall savings rate reaches approximately 35%, placing it among the highest globally.

-What makes a high savings rate an issue?

During the period of rapid growth, savings served as a vital source of domestic investment and contributed positively. At that time, surplus production was exported, fueling economic expansion. However, the circumstances have changed. South Korea can no longer depend solely on exports for long-term growth, particularly with the current trend of protectionist trade policies globally. Now, strong domestic demand must support exports, and private consumption is essential for domestic demand. Koreans save voluntarily and are also compelled to save through mechanisms such as the national pension system. Moreover, as observed last year, these savings frequently go abroad. If pension contribution rates increase, the savings rate will rise even more. Although the economy is currently experiencing growth, private consumption remains lively only for premium products, and the overall recovery is still inadequate.

-What makes South Korea’s savings rate so high?

Initially, longer life expectancy leads individuals to save more due to concerns about the future. Another reason is the pressure from high housing costs. Purchasing a home through a loan and paying it off can be considered a form of saving known as ‘housing.’ It is important to examine systems that enable younger generations to spend more before retirement, such as connecting housing pensions with the national pension scheme. Koreans frequently live in poverty and pass away with significant savings. In other words, they save in an inefficient manner.

◇ “The Objectives of the National Growth Fund Are Unlikely to Be Met”

-What is your assessment of the government’s National Growth Fund?

To establish such a fund, the government needs to clearly outline its policy objectives and realistically detail how to achieve them through investments. These elements remain unclear. The effectiveness of a policy fund relies on whether the managing body has responsibility and knowledge to develop long-term investment plans. However, the present fund structure is similar to previous ones, such as the ‘New Deal Fund,’ where funds are dispersed. Those receiving the money will likely opt for secure choices. Instead of taking risks for higher returns, they will manage the funds conservatively to prevent losses and collect fees.

-What is the best approach for the government to assist in the development of new technologies?

To boost national competitiveness, the government ought to identify industries or technologies vital for the future that the private sector finds challenging to invest in on its own. It is essential to provide strong, sustained support for these areas, even if they result in temporary losses. Naturally, the government should share the profits based on its level of investment. Even if four out of five supported sectors fail and only one succeeds, that single success should be a domain capable of supporting Korea. The fund must be designed to assume such risks.

-Is the National Growth Fund not adopting this method?

The National Growth Fund is ultimately managed by asset managers. They will make stable investments under the set conditions. Why should the government be in charge of such a fund? The private sector can handle this more effectively when it comes to resource allocation. For managing 150 trillion Korean won, it would be better to establish institutions similar to Singapore’s ‘Temasek’ or Israel’s ‘Yozma Fund,’ where specialists manage funds with long-term responsibility. The current method, where committees assess each case and allocate funds to managers, makes it difficult to achieve the desired objectives.

Leave a comment