Choi Won-seok, the CEO of “Jilgyeong,” a small-to-medium-sized company that produces and exports women’s products, recently carried out an experiment to settle around 10 million Korean won in export payments with an Indonesian trading partner using digital currency. Normally, export payments require converting Indonesian rupiah into US dollars, transferring them via an Indonesian bank to a Korean bank, and then converting them back into Korean won. This process is complicated, often taking up to a week, especially during holidays, with fees surpassing 4%. In this experiment, excluding transaction verification, the settlement was completed in under five minutes. The transaction utilized the Korean won stablecoin KORT (Korean Won Stablecoin), which was issued for testing in Indonesia by “Finiverse,” a startup established by Choi to simplify trade transactions. A stablecoin is a type of cryptocurrency designed to maintain a fixed value compared to traditional currency, such as “1 coin = 1 US dollar” or “1 coin = 1 Korean won.” Choi, who was recently interviewed, stated, “Although legal and tax restrictions under South Korea’s Foreign Exchange Transactions Act currently prevent full-scale issuance, we have already received many inquiries from Indonesian businesses.”

Although South Korea’s stablecoin legislation is still not finalized, nations such as Europe, Japan, and the United States have enacted relevant laws, broadening the applications. This has resulted in greater creation and application of Korean won stablecoins abroad, where regulatory frameworks are more relaxed. These are mainly utilized by companies needing international financial transactions, including trade settlements and institutional investors’ currency risk management.

◇Opportunity for Application in Trade Settlements for Products and Services

Leveraging blockchain-based stablecoins for international financial transfers leads to lower expenses and faster processing times than conventional banking methods. In contrast to fluctuating cryptocurrencies such as Bitcoin, stablecoins offer a more consistent value, making them more practical. Nevertheless, they are missing effective “safety protocols” like identity checks and anti-money laundering procedures, which are commonly used in the banking sector. Choi stated, “After regulations are completed, we anticipate resolving these challenges by working with traditional banks, which possess clear disclosure processes and anti-money laundering technology.” An additional drawback is the inability to qualify for tax exemptions (a zero tax rate) on export payments made using stablecoins.

Choi remembered a recent query from a Laotian business partner about dividing a $10,000 export payment because their bank lacked enough US dollars. He stated, “In countries such as South Korea, advanced foreign exchange markets typically don’t encounter these problems, but many developing nations have difficulty obtaining US dollars, leading to payment delays. Companies in these regions are especially keen on using stablecoin transactions.”

KORT is getting ready to launch on Indonesia’s biggest cryptocurrency platform, “NOBI,” once the regulatory framework is established. Lawrence Samantha, CEO of NOBI, who participated in a parliamentary session last month, stated, “We anticipate that Korean won stablecoins will be beneficial not only for merchandise trade but also for service trade transactions, including payments associated with Korean entertainment initiatives like concerts.”

◇ Increasing Adoption of “Coin Currency Hedging” in Korean Stock Investments

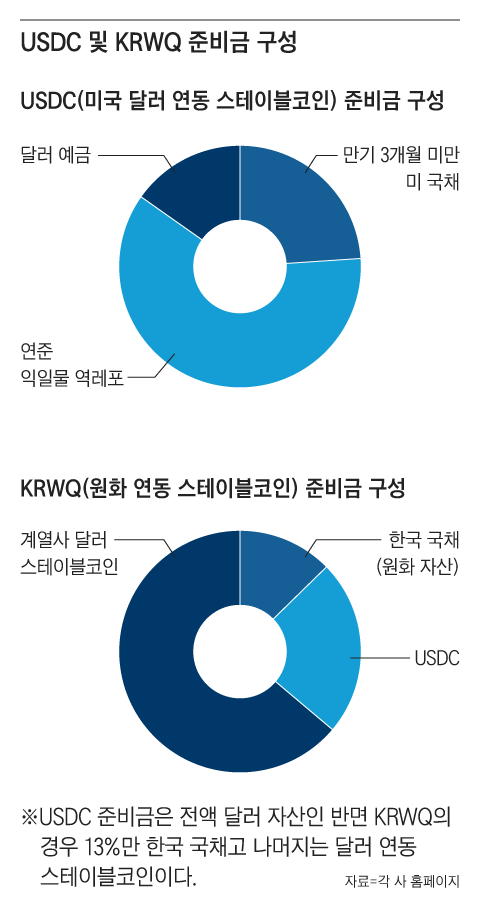

International investors are increasingly turning to offshore Korean won stablecoins as a means of protecting against the decline in value of the won. This growing trend began after the second half of last year, when the Korean stock market experienced a significant rise. The most commonly used stablecoin is KRWQ, an offshore Korean won stablecoin developed by blockchain companies IQ·Frax and available on institutional platforms such as EDX Market. As of the 3rd, its total supply reached around 1.1 billion Korean won. According to its website, each coin is tied to 1 Korean won, but it does not provide a corporate registration address, suggesting it functions as an “offshore coin.”

As per an analysis conducted by the virtual asset research company “Tigerly Research,” the average daily volume of KRWQ-based hedging for the Korean won after the second half of last year was approximately $1 million. Kim Gyu-jin, CEO of Tigerly Research, stated, “Although it is still modest, as foreign institutions show increasing interest in the Korean stock market, the usage of low-cost stablecoin hedging is anticipated to rise compared to traditional hedging products offered by financial institutions.” Vincent Chok, CEO of Hong Kong-based digital asset firm “First Digital Group,” which is working with KRWQ, mentioned to this newspaper, “Many institutions anticipate cost savings and enhanced efficiency if Korean won stablecoins are introduced in South Korea, considering the rising interest from overseas investors.”

◇Inadequate Counter-Illegal Activities Continue to Pose a Problem

However, KRWQ’s reserves contain approximately 13% in South Korean government bonds, with the rest held in US dollar stablecoins, which does not meet the requirements outlined in the stablecoin regulations of major countries. For example, the United States requires that stablecoin reserves be composed exclusively of cash and short-term government bonds in the currency that is pegged.

Anti-money laundering and tax evasion controls for stablecoins are also considered insufficient. A representative from a financial regulatory body stated, “It is impossible to regulate stablecoins utilized by foreign institutions outside of South Korea. Should domestic transactions rise, they could come under Korean regulatory oversight, but no applicable laws have been created yet.”

Leave a comment