South Korea’s initial single-stock leveraged exchange-traded products (ETPs) for Samsung Electronics and SK Hynix have begun to show indications of excessive activity since their launch, raising worries in the market that they might turn into “a large speculative area.” Although the government and financial regulators initially anticipated these products would shift capital from overseas-listed leveraged versions of Samsung and SK Hynix, thus helping stabilize the exchange rate, some analysts believe the real effect could be minimal.

◇First Day of Listing Features Trading Volume Double…“Essentially a Major Short-Term Trading Market”

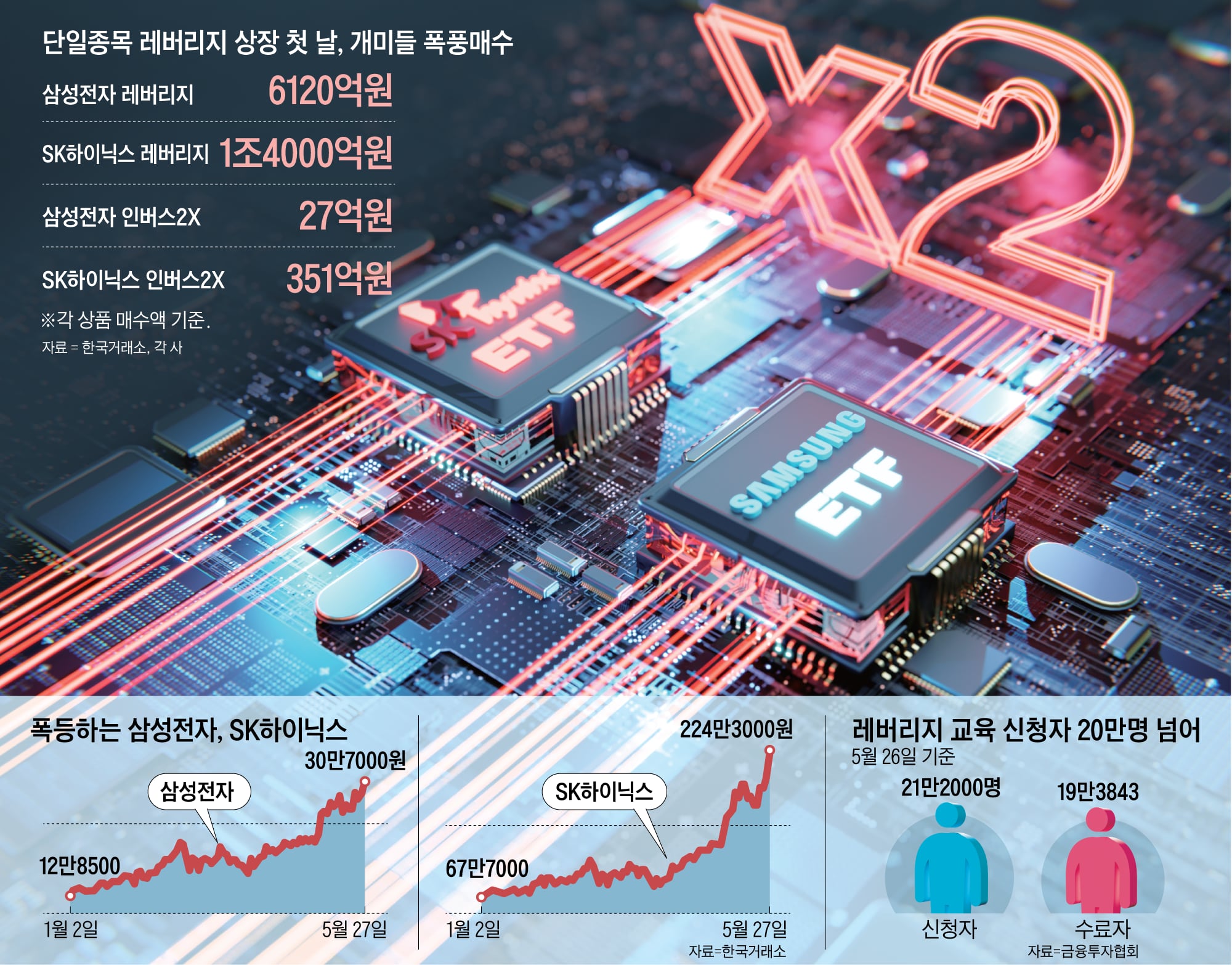

As per the Korea Exchange, the total trading volume of the 16 single-stock leveraged products that were listed the day before amounted to 417.38 million units. The overall number of listed units for these products was 206.13 million.

This suggests an average turnover rate of 202.5%. Turnover rate—defined as the ratio of trading volume to the total number of listed units—reflects the level of investor activity in trading the products. A rate above 200% implies that the entire listed volume was traded more than once within a single day, indicating a focus on intense, short-term “day trading.”

The highest trading volume was observed in SOL SK Hynix Futures Single-Stock Inverse, reaching 1,285.1%. Several other key products, such as ACE Samsung Electronics Single-Stock Leverage (263.9%), ACE SK Hynix Single-Stock Leverage (255.6%), TIGER SK Hynix Single-Stock Leverage (225.8%), and KODEX SK Hynix Single-Stock Leverage (223%), also had trading volumes above 200%.

Experts point out that single-stock leveraged products are naturally unstable and better suited for short-term investments rather than long-term positions. Nevertheless, they also caution that increased day trading activity might be prompted due to higher market volatility, as the KOSPI Volatility Index (VKOSPI) climbed 3.95% from the prior trading day, once more exceeding the 70 level.

A representative from the financial investment sector said, “Asset managers introducing these products are fundamentally forced to suggest individual stock investments to clients,” and noted, “In a market that is extremely unstable, there is a danger of increased speculative trading by retail investors.”

◇Questions Regarding the Impact of Currency Exchange Rates

One of the initial reasons the government had for launching these products was to maintain the exchange rate by shifting domestic investment interest away from overseas-listed Samsung and SK Hynix leveraged products towards the local market. Nevertheless, industry experts suggest that the real effect on exchange rates might be minimal, with short-term trading activity potentially increasing market fluctuations.

Certainly, local investors have significantly invested in CSOP Asset Management’s leveraged ETFs focused on Samsung Electronics and SK Hynix, which are listed on the Hong Kong stock exchange. As per the Korea Securities Depository, as of the 26th, the leading domestic investor in Hong Kong-listed funds was XL2CSOPHYNIX, a 2x leveraged SK Hynix ETF, holding assets valued at US$25.87 million. The seventh largest holding was XL2CSOPMSN, a 2x leveraged Samsung Electronics ETF, valued at US$12.66 million.

Market participants believe that although certain funds might move from Hong Kong-listed products to locally listed ones, the impact on exchange rate stability is expected to be small. A representative from the financial investment sector stated, “Arguing that these leveraged products lead to exchange rate volatility is unreasonable. Even if domestic investors purchase Hong Kong-listed leveraged Samsung products, the asset manager will ultimately buy domestic Samsung spot or futures. The money flows back into the local market, resulting in a minimal effect on the exchange rate.”

Critics also claim that merely introducing local products will not entirely shift overseas leveraged investment demand. Domestic single-stock leveraged products are subject to a 15.4% withholding tax on dividend income, comparable to current domestic ETFs. However, when annual financial income surpasses 20 million won, it falls under comprehensive financial income taxation, and even earnings above 10 million won are considered in health insurance premium calculations.

On the other hand, ETFs listed abroad are subject to capital gains tax following a $2,500 deduction, with a fixed rate of 22%, and they do not factor into health insurance premium calculations. A representative from the financial investment sector stated, “For investors with annual financial income surpassing 20 million won, tax implications offer minimal motivation to shift back to local products.”

Leave a comment